Feb 16 – Welcome home for instant market coverage brought to you by Reuters reporters. You can share your thoughts with us at [email protected]

List of possible sanctions against Russia (1117 GMT)

European shares regained some of their gains since faltering on Monday in hopes of calming tensions between Russia and Ukraine.

Register now to get free unlimited access to Reuters.com

Register

De-escalation is the most likely scenario for Unicredit’s chief economic officer in Central and Eastern Europe Dan Boksa, but targeted operations and territorial conquest have not been completely ruled out.

If he is right and tensions ease, the Russian economy may grow by 2-2.5% in 2023 and 2024, and the Russian Central Bank may start cutting interest rates in 2022, while the ruble may return to nearly 71 against the US dollar , he says. .

Buxa believes that the harshest measures on banks and gradual sanctions on oil exports are unlikely to be implemented. A ban on the use of the Swift financial messaging system would be harmful for up to a year, but it wouldn’t change the rules of the game.

But if Russia moves to invade Ukraine, “the peak-to-trough decline in GDP could be as high as 4%, the CBR could rise to about 15% and the Russian ruble could lose up to 30%,” he adds.

If tensions escalate to the targeted operations scenario, sanctions may target Russian investment vehicles, companies and individuals. This could include a ban on secondary market transactions with federal OFZ loans by US investors and a ban on the Nord Stream 2 energy pipeline.

In the worst case, territory invasion scenario, a ban on the use of Swift could be added to the sanctions list.

Buxa says the biggest economic risk in the event of a conflict in Ukraine is the fact that neighboring Central and Eastern European countries are dependent on imports of Russian natural gas and have gas stocks that cover less than two months of consumption.

He notes that “GDP growth in Central and Eastern Europe could slow by as much as 1.7 points in 2022.”

(Joyce Alves)

*****

EUROPE INC continues to stand up, analysts take notice (0943 GMT)

Europe’s fourth-quarter earnings season is going through its busiest week this month, and it looks like companies in the region continue to collect strong numbers.

According to the latest Refinitiv IBES weekly data, 62.5% of companies listed on the STOXX 600 that have already reported have exceeded market expectations, versus 52% in the usual quarter.

The analyst notes.

They now estimate that Europe Inc’s profit rose 58.6% to €116.5 billion in the fourth quarter, up more than two percentage points from last week’s estimate.

Revenues are now increasing by more than 20%.

Nine out of ten STOXX segments expect to see an improvement in earnings. Energy has the highest earnings growth rate at 385.5%, while real estate is the weakest, at -2.7%, per Refinitiv.

Further reading here:

European Gains: 2022 upgrades coming? Read more

Bank of America sees 10% rise in European bank profits Read More

Slightly burst gains optimism Read more

(Danilo Masoni)

*****

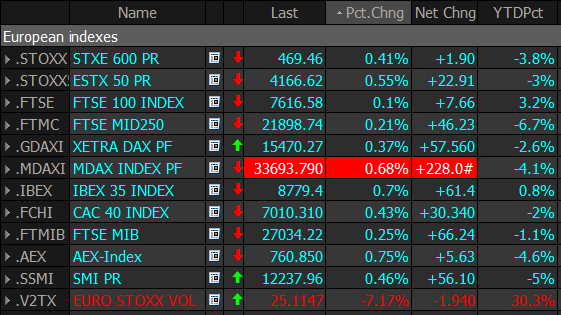

STOXX ON THE UP, WIN THE BEST DRIVES (0910 GMT)

European stocks opened higher on Wednesday, as the region teetered with an upbeat US shutdown on Tuesday amid lower tensions over an impending conflict between Ukraine and Russia.

Stokes 600 (.stoxx) The regional benchmark index rose 0.4% with almost all sectors in positive territory and earnings releases leading the biggest moves in both directions. Communication was a weak spot, down 0.8%.

Swedish medical technology group Vitrolife lost 10% after fourth-quarter net income fell nearly 70%. Shares of Swiss elevator and escalator company Schindler fell 4% after its fourth-quarter financials.

On the flip side, French lottery company La Francaise des Jeux rose 6.6% after increasing its revenue targets.

(Lucy Raytano)

*****

War, Peace and Inflation (0806 GMT)

February 16 was when Russia was supposed to invade Ukraine, according to the White House, but Moscow’s signals that it was withdrawing some troops massed on Ukraine’s border lifted Wall Street on Tuesday and sparked a sell-off in safe-haven Treasuries and German bonds.

Market gains extend into Wednesday – Japan’s Nikkei is up 2.2% and European bourses open higher, yet US stock futures are showing renewed signs of caution.

There are, of course, other ways to wage war. Ukraine blamed Russia for a series of cyber attacks on Tuesday. It should be noted that the Russian parliament asked President Putin to recognize the two eastern Ukrainian separatist regions backed by Moscow as independent.

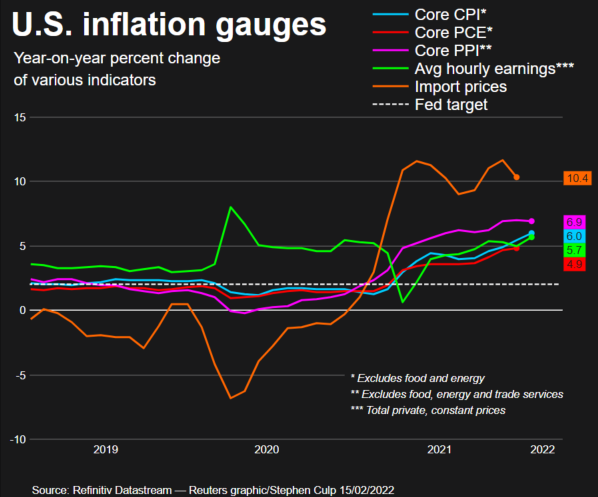

Economic data releases and central banks are also occupying the markets. Those hoping for signs of peak inflation will be dismayed by recent readings in the UK and US. British consumer prices rose at the fastest annual pace in nearly 30 years last month, up from a reading more in December

It comes a day after US data showed core factory gate inflation – producer cost excluding food and energy – posted its biggest gain in a year.

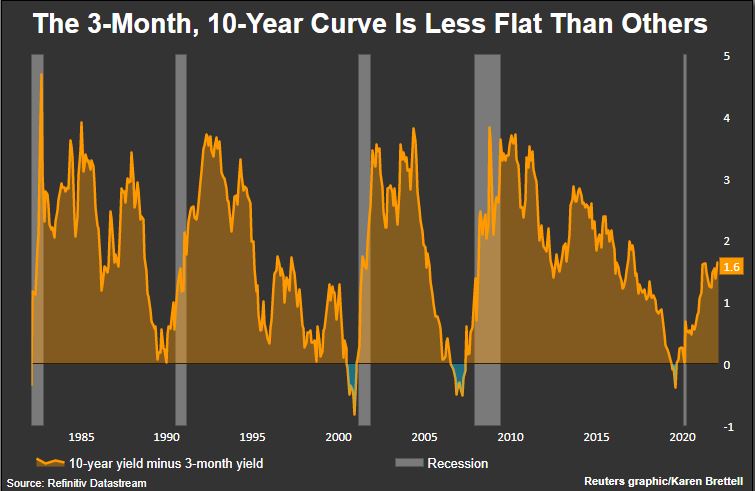

The potential for major interest rate hikes has flattened bond curves dramatically, with the gap between two to 10 year UK bonds turning negative to negative – the so-called inversion that often portends a recession.

The US Treasury yield curve sloped again on Tuesday as an easing of war fears lifted 10-year yields, but the day before it was the narrowest since mid-2020. For some, the state of the curve is a sign that central banks have pulled back. In its fight against inflation it must act faster as policy tightens to catch up.

All eyes are now on the minutes of the latest US Federal Reserve meeting. They can show whether policymakers will lean toward a half-point rate hike at the March meeting, or whether they would prefer to move faster as Fed bond holdings sell off to tighten financial conditions.

Key developments that should provide further guidance to the markets on Wednesday:

China’s inflation slows, leaving room for policy easing. read more

Schnabel-ECB’s, Villeroy’s eye end of the stimulus scheme

NATO defense ministers meet in Brussels for a two-day summit

US Retail Sales / Industrial Production / Inventory

20-year US Treasuries auction

– Minutes of the meeting from January 25 to 26

US earnings: Kraft Heinz, Cisco, AIG, Nvidia, Marathon

European earnings: Ahold, Alcom, Clariant, EDP, Standard Chartered, Heineken, Carrefour, Reckit Benckiser

(Sujata Rao)

*****

Europe sees gains, Ukraine remains in focus (0724 GMT)

European shares are set to rise slightly after Tuesday’s gains after signs of a possible escalation of tensions over Ukraine, although investors remain cautious about other possible developments in the crisis.

Euro STOXX 50 futures rose 0.6%, while contracts on the FTSE 100 rose 0.2% after data showed UK consumer prices rose at the fastest annual pace in nearly 30 years last month as inflation hit 5.5%. Read more

Meanwhile, US futures slipped slightly ahead of the Federal Reserve minutes later on Wednesday that may shape expectations about the speed at which the central bank will tighten policy.

Kiev appears to be blaming Russia for a cyber attack on Tuesday as US President Joe Biden warned that more than 150,000 Russian troops are still massed near Ukraine’s border. Read more

(Danilo Masoni)

*****

Register now to get free unlimited access to Reuters.com

Register

Our criteria: Thomson Reuters Trust Principles.

John Steinbeck was one of America’s most respected literary figures. Through classic works such as East of Eden, The Grapes of Wrath, and Of Mice and Men, he explored the complexities of human nature and the social challenges facing ordinary Americans. His writing remains a cornerstone of modern American literature.